Tips can help with compliance for contract worker regulations

Plan now to simplify year-end tax preparation

Veterinary hospitals commonly use contract workers throughout the year.

Spring and summer months especially bring opportunities for lawn services, maintenance and repairs and landscaping projects.

During the course of the year, most veterinary hospital administrators will engage the services of at least two or three individuals or companies who provide a variety of services, but are not hired as employees of the practice.

Be aware of rules

Since paying "under the table" is never a good idea, you should be aware and careful of the many rules controlling contract worker reporting.

First, you should be familiar with guidelines that suggest when an individual should be hired as an employee as compared to when that person can be deemed a contract worker. Although many times the relationship between practice and worker is very clear, other times the relationship may be a bit gray.

DVM Newsmagazine has previously published articles about the common-law rules the IRS uses as guidelines for determining when an individual is not a contract worker but an employee of the practice. Also, visit www.IRS.gov/contract workers.

Be conservative

In general, you may like to err on the side of conservancy if there is any question as to the person's relationship.

For example, if the individual is the sole worker (not associated with any company or does not have employees himself/herself) and works a substantial number of hours for your practice, you may wish to simply engage the person's services as a full-time employee.

If the individual is not, injury on the job may lead to troublesome debate about whose insurance is responsible, and whether worker's compensation is an issue.

What are some specific documents with which you must comply once you have decided the individual does fall within the realm of being a contracted worker or representing an unincorporated company providing services to your practice? Typically, service providers fall in the following list:

- Janitorial services

- Handymen/women

- IT and computer support companies or people.

- Landscaping and lawn services

- Snowplow service

- Electricians, plumbers, and HVAC workers.

- Attorney and law firm (whether unincorporated or incorporated).

- CPA, bookkeeping and non-CPA accounting services.

- Practice management advisors and consultants.

- Dry cleaners

- Relief veterinarians

- Veterinary specialists, either visiting your practice or for remote consultation purposes.

- Manure removal services

- Final arrangement service providers (crematories and cemeteries.)

We strongly advise obtaining the contractor's taxpayer identification number (TIN) before engaging services. If you forget, ask your bookkeeper to ensure that no new service provider is paid until the point you receive the TIN.

The best way to collect this information is to provide the contract worker a form W-9. This form requests the correct name of the worker and associated TIN. Furthermore, the form asks for the worker's certification that he/she is exempt from back-up income tax withholding.

As a reminder, Internal Revenue code section 6109 (a)(3) requires your practice (as the payer) to request the worker's correct TIN. The TIN must match the payee's name and be included on all information returns submitted to the IRS. The annually required information return typically used by the veterinary practices for reporting payments to contracted workers is the form 1099-MISC.

Be aware that payers who file information returns with missing, incorrect or mismatched TINs to the payee's name are subject to penalties for failure to file the correct information.

Get it upfront

Obtaining the form W-9 upfront is the best way to ensure that you have the correct reporting information at the point filing is required in January of the subsequent year. Immediately review the submitted form W-9 to assure all information is legible, since you will be relying on it later. In the event you have failed to obtain the information in the past, and do file incomplete or erroneous information returns, you will most likely receive notice from the IRS.

In this situation, contact your accountant immediately so that you correctly follow the rules in terms of follow-up. You may be required to immediately start back-up with tax withholding on the worker in question, if that person is still being paid for various work. The back-up withholding rate is 29 percent for 2004 and 2005. You will be responsible for making on-going requests to the worker for the TIN in order to avoid penalties.

Because payees may make mistakes in providing information to you about the correct name match with the TIN, make sure to keep all forms W-9 on file to prove the information you relied upon for preparation of information returns.

Name/TIN mismatches

A name and a TIN combination are incorrect if it can't be found in the IRS or Social Security Administration files. Mismatches happen when the individual's name does not match the TIN provided. TINs are not interchangeable with different names.

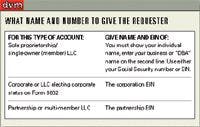

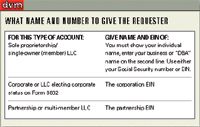

An employer identification number must be used for partnerships, corporations or limited liability companies. For individual names, a Social Security number must be used.

The IRS requires that you always provide the individual's name for sole proprietorship, even if the sole proprietor uses a "doing business as" (DBA) name.

Also, a sole proprietor may use a Social Security number or an employer identification number (EIN). However, sole proprietor must always furnish his/her individual name on the first name line of the W-9, regardless of whether they use a Social Security number or an EIN. A sole proprietor may provide a business' name (DBA) on the second name line, but must list the individual name first on the account with you.

Single-member LLC

The same rules hold true for a single-member LLC.

A single-member LLC is disregarded as a separate entity from the member-owner. The member must use his/her name as shown on the Social Security card with the LLC's name on the second line. Either the member's Social Security number or the EIN (if the LLC has one) can be used as the TIN.

Another useful resource for correct collection of names and TINs can be obtained from the IRS Web site (www.IRS.gov) through publication 1281, "Back-up Withholding on Missing or Incorrect Name/TINs."

When preparing information returns at the end of the year, avoid abbreviating company names whenever possible. If you know a company has changed its name, ask if the IRS is informed of the change. The IRS and the Social Security Administration must be informed of any name changes by the company in question.

Many service providers are unaware what business format they operate in (corporation, limited liability company, sole proprietorship). For this reason, it is advisable to obtain a form W-9 from every contracted service provider, even if they attest to being incorporated.

It never hurts to have the extra documentation on file.

Keep all the completed forms W-9 filed in one easy-to-access filing location. Usually, your bookkeeper will want to have control of these documents to expedite form 1099-MISC processing at year-end.

QuickBooks and other practice bookkeeping programs allow input of EINs and TINs with the vendor's name, so the forms can be processed at year-end through the software program.

High cost

Although record keeping requirements are a burden, be aware that the cost of not doing so can be quite significant.

The IRS provides for three distinct categories of penalties that relate to failure to file required information returns and payee statements. These penalties range from a low of $15 per return up to a yearly maximum penalty of $250,000 in the case of failure to file correct information returns and up to a maximum of $100,000 per calendar year for failure to furnish correct payee statements or comply with other information reporting requirements.

None of these penalties includes penalties that might be attributable to intentional disregard of the rules.

All in all, the simplest way to approach contract worker reporting requirements is to make every effort to obtain a signed form W-9 before the individual ever begins work for your practice.

Doublecheck the information on the form for legibility and a match of number and name, before filing the form in an easily remembered location. Make your life simple for January, up to 12 months in the future.